Should I Pay Off My Mortgage Before Retiring?

No it's not required. But whether you carry a mortgage into retirement can make or break how comfortable that retirement actually feels. It all comes down to how big that payment is, what your income looks like when you stop working, and whether you've planned for it.

If you're weighing whether to put extra money toward the mortgage or into investments, that's a slightly different question and one worth thinking through carefully. Here's a breakdown of whether to pay off your mortgage or invest.

The Honest Answer Most People Aren't Told

You don't have to be mortgage-free to retire. Plenty of people do it. But there's a big difference between retiring with a mortgage on purpose with savings, a plan, and income to support it and retiring with a mortgage by accident, because life got busy and the balance never really moved the way you hoped.

I've worked with clients on both sides of this, and the ones who struggle aren't always the ones with the biggest mortgage. They're the ones who didn't plan around it.

What I've Seen With Real Clients

The clients who retire with a mortgage and do just fine? They planned for it. They have retirement savings, solid income coming in, and the mortgage payment is one line on a budget they've already run the numbers on.

The ones who have a harder time are usually dealing with a mix of things:

Their income drops sharply at retirement especially if they're mostly relying on government benefits like CPP and OAS

They didn't build up much in retirement savings alongside the mortgage

Their mortgage balance hasn't gone down the way they expected, because they kept borrowing against their equity over the years

That last one is really common. People use their home equity for renovations, kids' tuition, a car and by the time retirement is around the corner, the balance is sometimes higher than when they bought the house. That's when carrying a mortgage into retirement gets stressful.

The Factors That Actually Matter

When I sit down with someone to figure out whether paying off before retirement should be their goal, here's what I'm actually looking at:

Does Being Mortgage-Free Before Retirement Actually Matter to You?

This one matters more than people expect. For a lot of people, being mortgage-free isn't just a financial goal it's peace of mind. It's waking up in retirement knowing your house is yours, no payment due, no bank to answer to. That's worth something real. If that's what you're after, that's a completely valid reason to make it the goal.

Are You Planning to Stay in Your Home Through Retirement?

If you're planning to stay in your home as long as possible, paying it off makes a lot of sense. Your home becomes part of your retirement, and owning it outright gives you options you can downsize later and keep more of the proceeds, or just enjoy the flexibility that comes with no mortgage payment eating into a fixed income.

How Much Income Will You Actually Have When You Stop Working?

This is where the math gets real. When you stop working, your income drops sometimes a lot. A mortgage payment that felt manageable on a $150,000 household income can feel suffocating on CPP, OAS, and some RRSP withdrawals. The smaller your expected retirement income, the more important it is to have that payment gone before you get there.

Why Feeling Behind Isn't a Willpower Problem

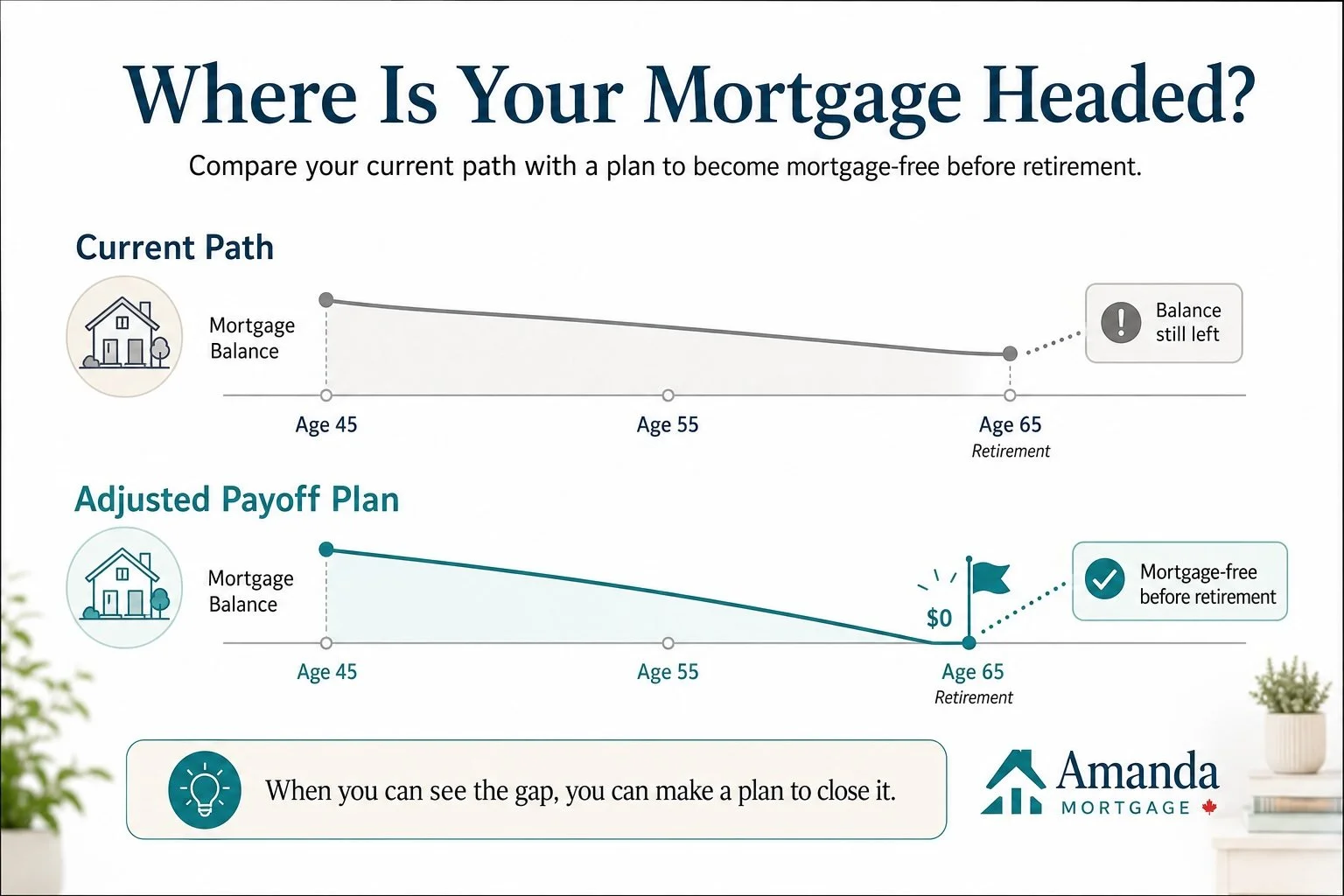

Here's something I tell clients regularly: if you earn a decent income, you've made your payments, and you're still not where you thought you'd be with your mortgage that's usually not a discipline problem. It's a visibility problem.

Most people have never actually looked at what their mortgage is going to look like in 10 or 15 years on the current path. When we pull that number up and put it beside where they want to be at retirement, suddenly there's something to work with. Once you can see the gap, you can make a plan to close it.

And in a lot of cases, it doesn't take earning more money. It takes making your income work smarter against the balance you already have. These strategies for paying off your mortgage faster in Canada are a good place to start.

What Should You Do?

If you're in your 40s or early 50s and you're not sure where your mortgage is going to land when you want to retire, the most useful thing you can do right now is find out. Not guess actually look at the numbers.

From there, you can decide whether paying it off before retirement is the right goal for you, and build a plan around it. A Mortgage Momentum Plan can show you exactly where you're headed and what it would take to get to mortgage-free before you stop working using the income you already earn.

That might mean a small cash flow adjustment. It might mean restructuring how your income flows through the mortgage. One client I worked with took what looked like a 30-year mortgage and got it on track for something much closer to 13 years — see how turning a 30-year mortgage into a 13-year plan actually works. But it all starts with seeing your actual number.

What If You Can't Pay It Off Before You Retire?

This is the question most people are actually afraid to ask. And the honest answer is: it's not a disaster, but it does require a plan.

If retirement is 10–15 years away and your mortgage is nowhere near paid off, the first thing to look at is whether the current structure is working against you. A lot of clients I meet have been making payments faithfully for years but haven't seen the balance move the way they expected. That's often a structure problem, not an income problem.

There are also a few practical options worth knowing about:

Accelerated payment schedules can shave years off a mortgage without dramatically changing your monthly budget

Refinancing to consolidate higher-interest debt can free up cashflow that goes directly against the mortgage

A mortgage review can identify whether you're on the most efficient payoff path given your current income

None of these require earning more. They require looking at whether your money is working as hard as it could be. If you're in your late 40s or early 50s and feeling behind, that gap is very often closeable — you just need to see the actual numbers first.

Common Questions About Paying Off Your Mortgage Before Retiring

Is it better to pay off your mortgage or save for retirement?

It depends on your expected investment returns, and how close you are to retiring. For most people in Ontario, carrying a high mortgage balance into retirement on a fixed income is riskier than it looks on paper. The better question is whether you can do both, and that usually comes down to how your income is flowing through the mortgage right now.

What happens if I still have a mortgage when I retire?

You can still retire with a mortgage. The key is whether your retirement income (CPP, OAS, pension, RRSP withdrawals) can comfortably cover that payment. According to Statistics Canada, a significant portion of Canadian retirees rely primarily on CPP and OAS, which averaged around $14,000–$21,000 per year combined. A $1,500/month mortgage payment on that kind of income is a very different conversation than it was when you were earning $130,000 a year.

How much should I have paid off before I retire?

There's no universal number, but a practical rule of thumb is: your mortgage payment should be no more than 25–30% of your expected monthly retirement income. If that math doesn't work on your current trajectory, it's worth looking at your options now rather than at 63.

Can I pay off my mortgage faster without earning more money?

Yes. In many cases, the issue isn't income, it's structure. How your income flows through the mortgage, the timing of your payments, and how your interest is calculated can all make a significant difference to how quickly the balance actually drops. That's typically where the biggest gains are found.

Key Takeaways

You don't have to be mortgage-free to retire but it matters a lot how big that payment is relative to your retirement income

The people who struggle most in retirement with a mortgage are those who didn't plan around it, not those who carry it intentionally

Whether to pay it off before retiring depends on your goals, your plan for the house, and what your income will realistically look like when you stop working

If you feel behind, it's usually a visibility problem, not a willpower problem you just haven't seen the full picture yet

The first step is finding out exactly where your mortgage is headed, so you can decide whether you need to change course