Can I Refinance My Mortgage to Pay Off Debt?

The answer is yes. In most cases, you can refinance your mortgage to pay off other types of debt.

If you're struggling with credit card balances, lines of credit, or other high-interest debt, you might be wondering if you can refinance your mortgage to pay it all off.

But whether it's the right move depends on your situation, your goals, and most importantly, what happens after the refinance.

As a mortgage agent, I've helped many homeowners use their home equity to simplify their finances and reduce stress. The biggest difference between the people who succeed and the people who end up back where they started isn't the refinance itself. It's having a plan.

How Mortgage Refinancing for Debt Consolidation Works

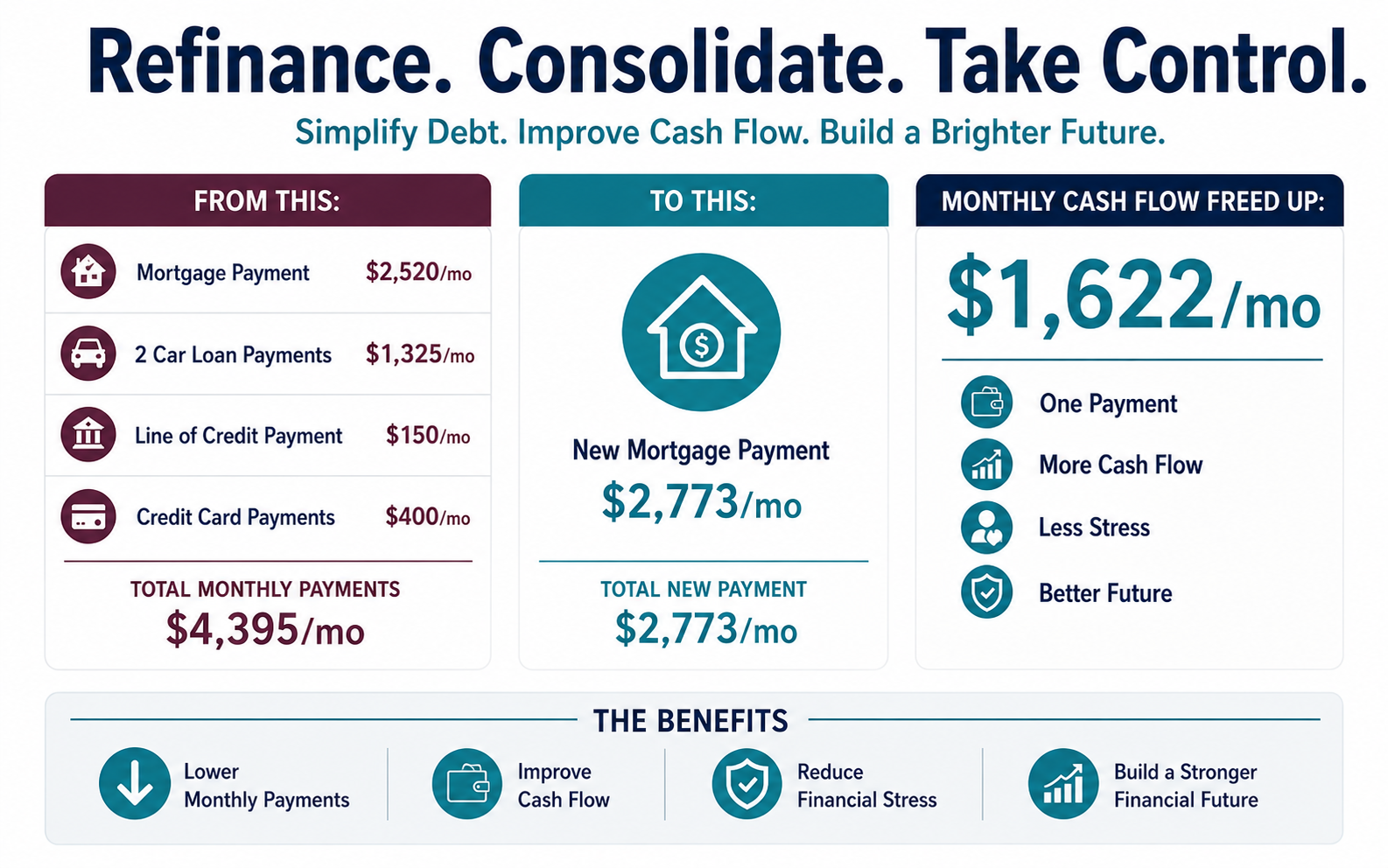

When you refinance your mortgage, you may be able to borrow against the equity you've built in your home and use those funds to pay off higher-interest debts such as:

Credit cards

Lines of credit

Personal loans

Car loans

Other unsecured debt

Instead of juggling multiple payments at different interest rates, everything is rolled into one mortgage payment, often at a much lower interest rate.

For many homeowners, this can significantly improve monthly cash flow and make managing finances much easier.

Is Refinancing to Pay Off Debt Usually a Good Idea?

In my experience, if someone has accumulated a significant amount of debt outside of their mortgage, refinancing to consolidate that debt is often a smart move.

Of course, every situation is different. Sometimes qualification rules or income limitations mean we can't consolidate everything. In those cases, we look at other options and see if consolidating part of the debt can still create meaningful improvements.

The goal isn't simply to refinance. The goal is to put you in a better financial position than where you started.

The Concern I Hear Most Often: "Won't I Just Be Extending My Debt?"

This is probably the biggest hesitation homeowners have.

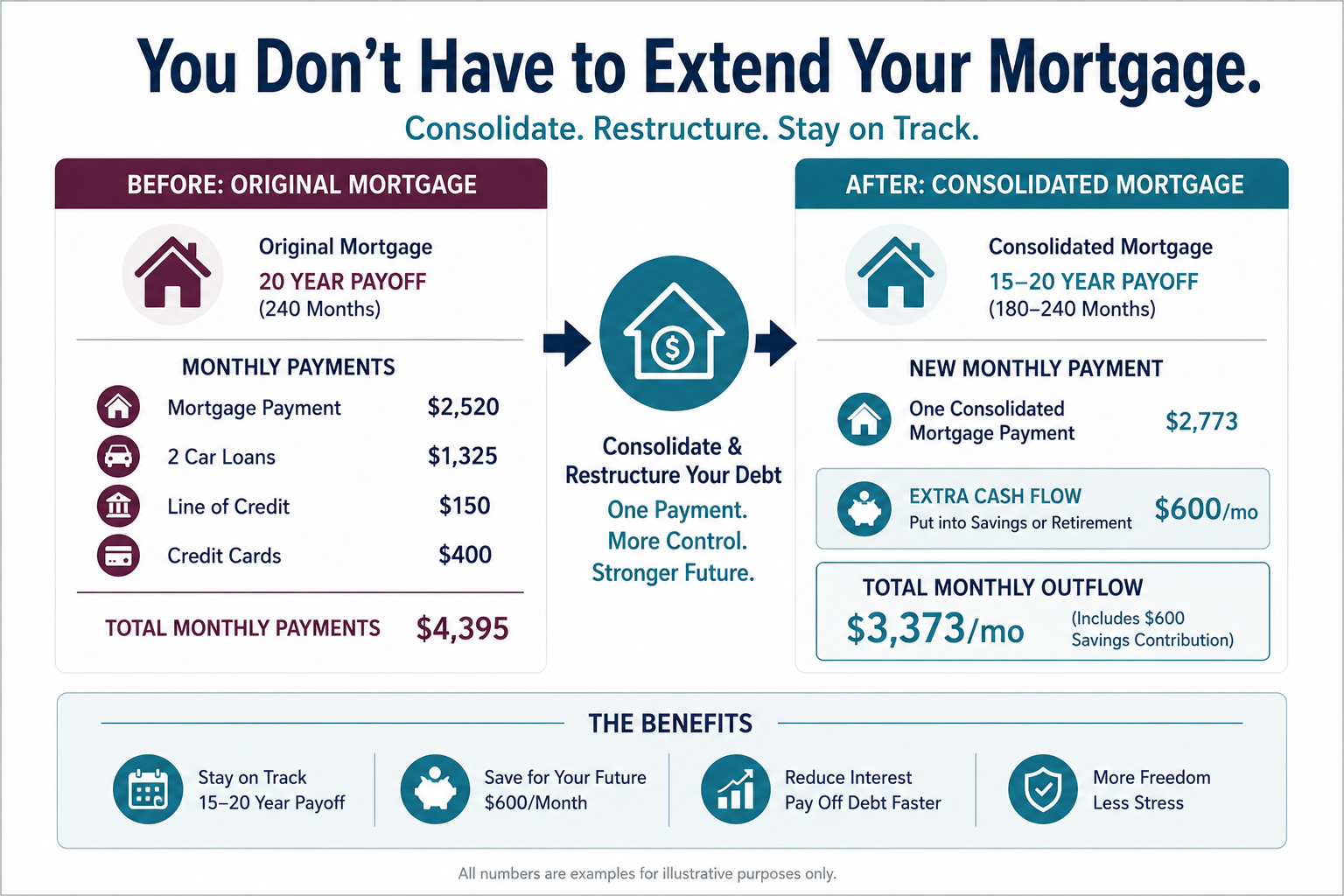

Someone might have 20 years left on their mortgage, refinance, and suddenly they're looking at a 30-year amortization. It feels like they've added another decade of payments.

On paper, that can happen.

But it doesn't have to stay that way.

A Longer Amortization Doesn't Mean You Have to Stay There

One strategy I often use is combining debt consolidation with what I call the Cashflow Freedom Plan - a structured approach to refinancing that focuses on more than just the rate.

By eliminating high-interest debt payments, many clients suddenly free up hundreds or even thousands of dollars each month. Instead of letting that money disappear into everyday spending, we create a strategy to put it back toward the mortgage.

In many cases, clients can match their original payoff timeline or even pay off their mortgage earlier than they would have before refinancing.

That's why I don't just look at the interest rate or payment. I look at the entire picture.

The Biggest Myth About Refinancing Debt

One myth I wish homeowners would stop believing is that refinancing automatically means you're stretching your debt out forever.

That's only true if nothing changes after the refinance.

The real danger isn't extending the amortization.

The real danger is refinancing your credit cards into your mortgage and then filling those credit cards back up again.

If that happens, you've simply traded one problem for a bigger one.

That's why I spend time talking about spending habits and creating a realistic plan. Debt consolidation works best when you address both the financial math and the behaviour behind it.

You have to be honest with yourself about your spending patterns if you want the refinance to create lasting change.

My Favourite "Aha" Moment With Clients

One of the most rewarding parts of my job is watching clients realize just how much monthly cash flow they can free up.

That breathing room changes everything.

Instead of living payment to payment, they suddenly have options.

They can:

Pay down their mortgage faster.

Build an emergency fund.

Start investing for retirement.

Increase existing savings.

Feel like they're finally getting ahead instead of falling behind.

Many people don't believe that's possible until they actually see the numbers.

My role is to show them the path. It's always their decision whether they choose to take it.

Success Isn't Just About Paying Off Debt

For me, success isn't measured only by how much debt disappears.

It's measured by how my clients feel after the refinance.

When someone tells me they finally feel like they can breathe again, that they're sleeping better, or that they finally feel in control of their finances, I know we've accomplished something meaningful.

Reducing financial stress often improves every other area of life.

It also prepares people for the unexpected. If something comes up in the future, they're in a much stronger position to handle it without immediately relying on more debt.

What Happens If You Do Nothing?

I often encourage clients to ask themselves a simple question:

What is the alternative?

If nothing changes, many homeowners continue struggling with high-interest debt, make only minimum payments, and slowly watch their balances grow.

Eventually, that stress can lead to missed payments, damaged credit, and even fewer options available down the road.

Taking action before reaching that point often creates far more opportunities than waiting until the situation becomes urgent.

Should You Refinance Your Mortgage to Pay Off Debt?

For many homeowners, the answer is yes.

But refinancing should never be viewed as a quick fix.

It should be part of a bigger strategy that improves cash flow, reduces stress, and helps you build better financial habits going forward.

The right debt consolidation plan doesn't just lower your payments. It gives you the opportunity to take control of your finances and create a future where you're no longer relying on debt to get by.

That's the outcome I want for every client I work with.