Is the Lowest Mortgage Rate Always Best in Canada?

No. At least not when it comes to your total cost. And the reason why is something most banks will never bring up. The rate tells you what you're paying per day to borrow money. What it doesn't tell you is how many days you'll be paying it. And that second number can matter just as much to your total cost. On a $500,000 mortgage at 4.1%, the right structure can save over $130,000 in interest and get you mortgage-free more than 10 years sooner, for just $33 more per month than your current payment. Same rate. Very different outcome.

Most people shopping for a mortgage are focused almost entirely on one number: the rate. And that makes sense, because it's what banks lead with. It's what comparison sites are built around. It's the number that gets texted to your group chat when someone gets approved.

But rate is only half the equation. The other half is how long you carry the balance. And that half gets almost no attention at all.

Why Everyone Is Focused on the Wrong Number

When a bank offers you a mortgage, the only tool they have is the rate (plus maybe some cash back or rewards points). So that's what the conversation is about. Lower rate, lower payment, better deal. It's clean, it's simple, and it's incomplete.

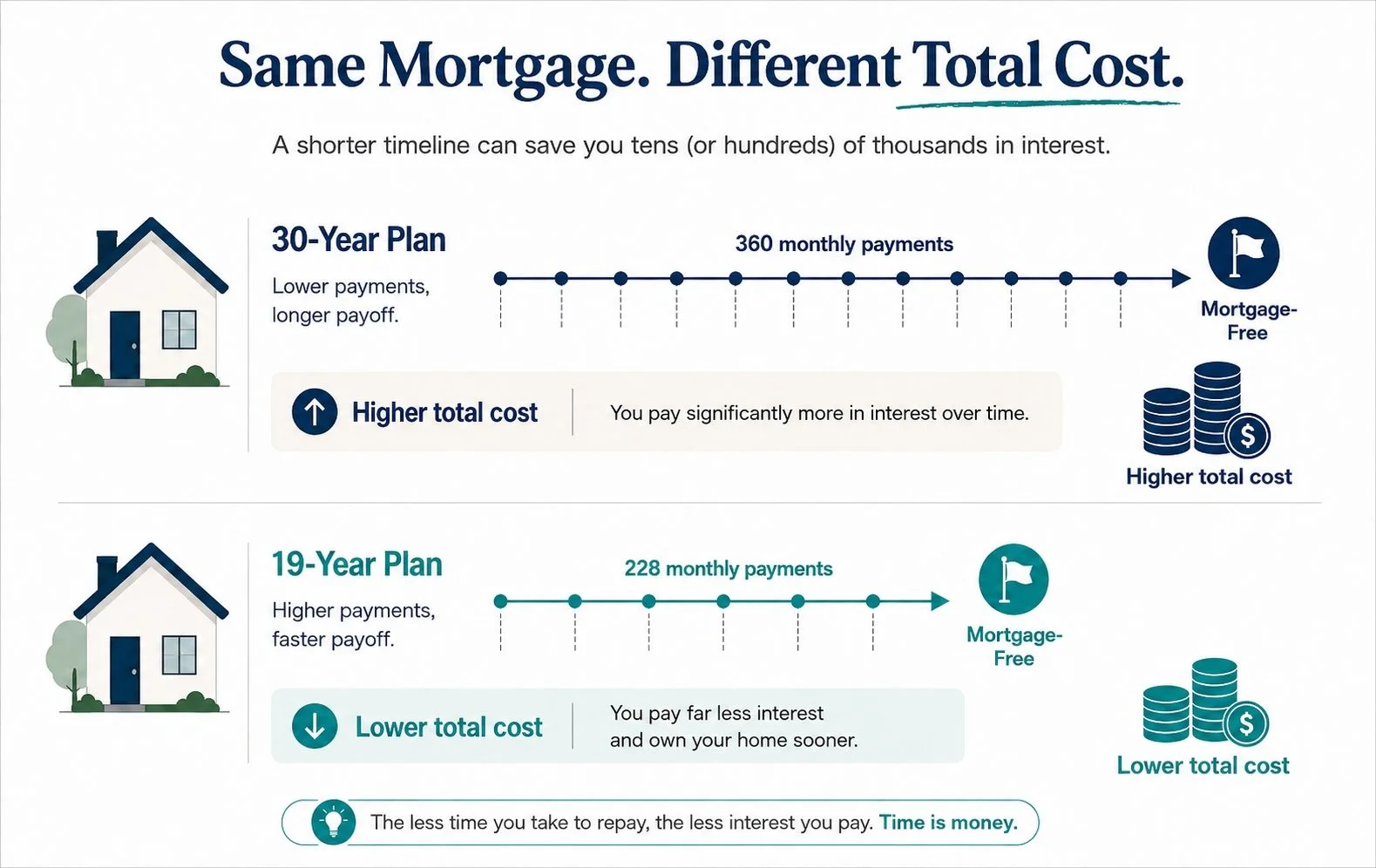

Here's the part that doesn't get discussed: a mortgage at a slightly lower rate, carried for 30 years, can cost far more in total than a mortgage at a slightly higher rate that gets paid off in 20.

The rate tells you what you're paying per day to borrow the money. It says nothing about how many days you'll be paying it.

A useful way to think about this is the contractor analogy.

Why the Cheaper Option Can Actually Cost You More

Imagine you're hiring a contractor to renovate your kitchen. One contractor charges $400 per day. Another charges $450 per day. On paper, the cheaper contractor is the obvious choice.

But what if the $450 contractor finishes the job a full week early? Suddenly the math changes. The "more expensive" contractor ends up costing you less in total, because they were on the clock for fewer days.

Mortgages work exactly the same way. The rate is the daily cost. The amortization is how many days the clock runs. You can have a great rate and still pay far more than you need to if the clock runs for 30 years.

This is why I talk about mortgage structure differently than most. The goal isn't just a competitive rate. The goal is to shorten how long the clock runs, using the income you already have.

What the Numbers Actually Look Like

Here's a real comparison using a $500,000 mortgage at 4.1% with BMO: $8,500 monthly income, $7,730 in monthly expenses, and $770 left over each month.

Staying Put: 30-Year Mortgage at $2,406/Month

Total interest paid over 30 years: $366,149. That's the default. Nothing wrong with it, it's just a very long time to be paying interest on a balance that barely moves in the early years.

Accelerated Payments: $2,607/Month

Switching to accelerated bi-weekly payments brings the mortgage-free date forward to 25 years 10 months and reduces total interest to $307,518, a saving of about $58,000. It costs $201 more per month in payments.

Cash-Flow Structure: $2,439/Month

Here's where it gets interesting. The cash-flow structure costs just $2,439 per month (minimum payment), only $33 more than the current payment. But it gets the mortgage paid off in 19 years 8 months, with total interest of $236,007. That's $130,142 in interest saved compared to doing nothing, and it happens automatically.

The equivalent borrowing cost drops from 4.10% to 2.78%, not because the rate changed, but because the balance is reduced faster. The rate tells you what you're paying per day. The structure determines how many days you pay it.

The full explanation of how that works mechanically is covered in how to pay off your mortgage faster in Canada. The short version: instead of your paycheque sitting in a chequing account until payment day, it immediately reduces your mortgage balance. Every dollar not spent on bills is working against the mortgage automatically, without you having to think about it.

Why Extra Payments Are Not the Same Thing

When people hear this, the first question is usually: couldn't I just make extra payments on my current mortgage?

It's a fair question. And extra payments do help. But they have real limitations that this structure doesn't.

With most traditional mortgages, extra payments are capped at 10 to 20% of your starting balance per year depending on the lender. Some only allow them on specific dates. And once that money goes into the mortgage, it's difficult to get back if you need it. A job change, an unexpected repair, a family situation. The money is locked into equity and accessing it means going through a refinance.

The cash-flow structure handles this differently. The extra progress happens automatically, every month, based on how your income flows through the account. And if you need access to the money, it's there. You're not locked in. One difficult month doesn't derail the plan. You adjust, and progress resumes when things normalize.

This is what makes flexibility a real feature rather than a marketing phrase. See how the Mortgage Momentum Method works.

Who This Is and Isn't Right For

This structure works well for homeowners who have equity in their home, fairly steady income, and some breathing room in their monthly budget. If you generally have money left over at the end of the month, even modestly, this approach puts that gap to work automatically.

Where It Works Best

The structure does the heavy lifting. You don't need to be the kind of person who manually moves money around or tracks extra payments on a spreadsheet. You just need to be someone who isn't spending every dollar that comes in.

Where It Is Not the Right Fit

If credit issues mean you don't currently qualify, this conversation is a bit premature. If income and expenses are perfectly matched with nothing left over each month, there's no surplus for the structure to use. And if having access to a growing line of credit is genuinely tempting rather than reassuring, this setup can work against you. I'll always tell you honestly if the fit isn't right. What Is a Manulife One Mortgage goes into more detail on the product side and who it tends to suit.

Common Questions About Rate vs. Mortgage Structure

Is a lower mortgage rate always the better deal?

Not necessarily. Rate matters, but it's one variable in a larger equation. If a lower rate comes with a structure that locks your money away, limits prepayments, or keeps you carrying the balance for 30 years, the total cost can still be higher than a slightly different rate with a structure built to shorten the timeline. Always look at total interest paid alongside the rate.

Do I need to earn more to make a 19-year timeline realistic?

No. The clients who see this kind of result aren't earning more than they were before. They've changed how their existing income flows through the mortgage. Same paycheque, different structure, significantly different outcome over time.

When is the right time to look at restructuring?

Anytime! But their could be a penalty to move your mortgage mid term (bit it’s often still worth it). At renewal time is best. That's when you can reassess lenders, terms, and structure without penalty. If your renewal is coming up in the next 12 months, it's worth having the conversation now rather than just signing what arrives in the mail. A mortgage renewal is one of the most underused opportunities homeowners have to change direction.

What if I have a few bad months and can't keep up the pace?

Nothing breaks. The structure is designed around real life, not a perfect budget. If a month is tight, you adjust. Progress resumes automatically when things normalize. That's the whole point of building flexibility in rather than locking it out.

Key Takeaways

Rate is what you pay per day to borrow. How long you carry the balance determines how many days you pay it. Both matter, and most mortgage conversations only cover one

On a $500,000 mortgage at 4.1%, a cash-flow structure saves $130,142 in interest and cuts over 10 years off the timeline

The contractor who costs more per day but finishes early can cost less in total. Mortgages work the same way

Accelerated payments help, but they are limited by your lender, and lock your money away. A cash-flow structure does more, automatically, with full flexibility to access funds if you need them

Renewal time is the best moment to look at restructuring. If yours is coming up, it's worth understanding your options before you sign