What Is a Manulife One Mortgage?

A Manulife One mortgage is an all-in-one mortgage and banking account that combines your mortgage, line of credit, and daily banking so your income automatically reduces your mortgage balance, helping you save interest and pay off your mortgage faster.

If you’ve been researching ways to pay off your mortgage faster, you may have come across something called a Manulife One mortgage.

It’s often described as:

an “all-in-one mortgage”

an “offset” mortgage

a mortgage combined with a line of credit

or a different way to manage debt and cash flow

But those explanations don’t always make it clear how it actually works, or whether it’s even right for you.

Especially when most people are used to thinking about mortgages, banking, and savings as completely separate things.

This article will walk through what a Manulife One mortgage is, how it’s different from a traditional mortgage or HELOC, and why it’s often used as the foundation for paying off a mortgage faster.

What Is a Manulife One Mortgage?

A Manulife One mortgage is a readvanceable mortgage offered by Manulife Bank of Canada that combines:

your mortgage

a revolving line of credit

and your everyday banking

into one integrated account.

Instead of having:

a mortgage at one institution

a chequing account somewhere else

savings accounts sitting separately

It brings everything together so your money can work more efficiently.

It’s one account where your income, bills, savings, and mortgage all interact, rather than acting like strangers who don’t know each other.

Simple example:

You deposit $4,000 into your Manulife One

You spend $3,000 on bills over the month

The remaining $1,000 reduces your mortgage balance and lowers your interest cost for part (or all) of the month

If you need that $1,000 at any time, you can access it.

Your money isn’t locked away the way extra payments often are with traditional mortgages.

How Is Manulife One Structured?

It is set up as a custom borrowing limit, secured against your home.

That limit is based on your home value, income, credit, and overall financial picture (similar to qualifying for a traditional mortgage).

Inside that limit, you can have:

fixed mortgage portions (with set terms and payments)

a revolving portion that functions like a line of credit

everyday banking features such as bill payments and direct deposit

As you pay down the mortgage principal, your available credit automatically increases. This is known as automatic readvancing.

Manulife One vs. a Traditional HELOC

Homeowners often ask whether Manulife One is “just a big HELOC.”

It’s not.

Manulife One

Custom mortgage structure with automatic readvancing

Integrated daily banking

Flexible minimum payment requirements

Fairer prepayment penalty calculations

No branch visits required (online setup and management)

Mortgage agent/broker support and guidance

Traditional HELOC

Often requires separate mortgage and banking accounts

Re-advancing may not be automatic or available at all

Minimum monthly interest payments are required

Banking fees and minimum balances often apply

Typically set up and managed in-branch

Exact features vary by lender, but these are the most common structural differences.

Manulife One is not a strategy by itself.

It’s a tool that allows a specific strategy to work properly.

Because:

income can be deposited directly into the account

interest is calculated on the daily balance

leftover money automatically reduces the mortgage

It uses your existing income more efficiently.

This is why it’s often used as the foundation for my cash-flow-based mortgage approach, which focuses on:

reducing interest earlier

accelerating principal paydown

preserving flexibility

This shifts more of your money toward principal much sooner, which is what actually shortens the life of a mortgage.

Read more about how a cash-flow mortgage works.

Does a Manulife One Mortgage Actually Save Money?

If used properly, yes.

There’s nothing “magical” happening.

The savings come from three very practical factors:

consolidating debt at a lower secured rate

using savings efficiently to reduce interest instead of earning minimal savings interest

applying excess cash flow to debt automatically over time

The results can look impressive, but they come from basic math and efficiency, not risk or leverage.

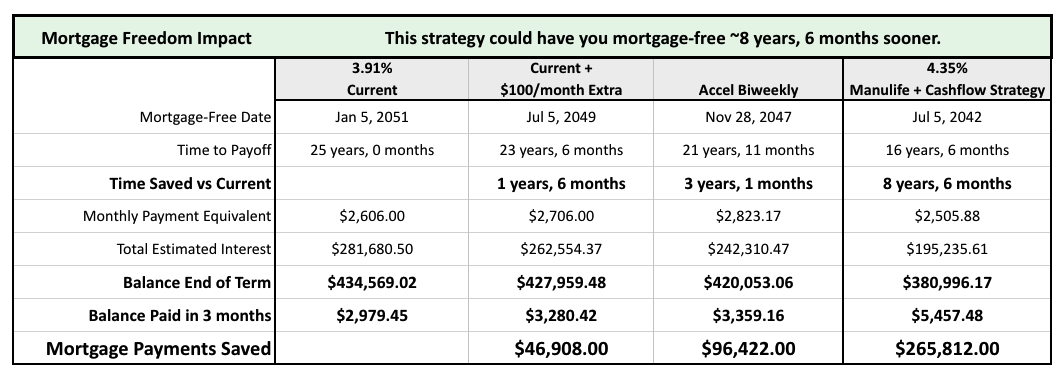

Here’s a comparison of a traditional $500,000 mortgage at 3.91%.

You can see that the Manulife One + cash-flow strategy saves the most time and interest in this example, where the household has approximately $1,000 left each month after all expenses are paid.

What About the Monthly Fee?

Manulife One has a monthly account fee (currently $16.95, or $9.95 for clients 60+). Sometimes brokers can get this waived for a limited time.

This fee:

covers unlimited daily banking

replaces many separate banking fees

is often outweighed by interest savings

As the saying goes, this isn’t about “stepping over dollars to pick up pennies.”

When used properly, the efficiency gains typically far exceed the monthly cost.

Is Manulife One Risky?

Used improperly, any credit product can be risky.

Used and set up properly, Manulife One is often less risky than juggling:

multiple high-interest debts

separate banking accounts

rigid mortgage structures

A proper setup typically includes:

fixed mortgage portions

a flexible portion for cash flow

spending expectations

annual check ups

The goal isn’t to encourage debt, it’s to manage debt more intelligently.

Common Mistakes With Manulife One

1. Putting the entire mortgage balance into one giant line of credit

This is one of the most common mistakes, and it’s usually not recommended.

In most situations, placing the entire mortgage balance into the revolving (HELOC-style) portion, exposes you to unnecessary interest costs.

Instead, Manulife One should be structured intentionally, typically with fixed mortgage portions and a flexible portion designed around your cash flow.

The structure should match how your money actually moves, not just maximize available credit.

2. Using available credit faster than you can pay it down

I’m not here to tell anyone how to live their life or how to spend their money or equity.

What I can share is a common pattern I’ve seen.

For people who tend to use available credit as soon as they have access to it, Manulife One may not feel like a good experience.

In those situations:

the balance can increase instead of decrease

progress feels slower or non-existent

frustration builds because it doesn’t match the “pay it off faster” expectation

This is often why you’ll hear someone say they “didn’t like” Manulife One.

In most of those cases, it’s not because the mortgage itself didn’t work.

It’s usually because:

the structure wasn’t set up properly for their behaviour or cash flow, or

they weren’t clearly shown how to use it, or

it simply wasn’t the right fit for someone who is tempted with large amounts of readily available credit

Manulife One works best when there is some spending discipline, surplus cash flow, and a clear structure in place.

3. Not planning for how available credit grows over time

As the balance is paid down, available credit automatically increases.

That flexibility is powerful, but only when paired with:

spending discipline

a defined structure

and an understanding that you will have access to more credit as your balance goes down

Part of my role is helping clients decide how that growing equity fits into their long-term plan, so it doesn’t turn into unnecessary debt later.

This is where the cash flow first framework matters.

We don’t design the structure around the maximum limit you qualify for, we design it around your income, expenses, and behaviour.

This is also why working with someone who understands how to structure Manulife One properly matters more than simply getting approved for it.

Why Flexibility Matters (When Life Happens)

One of the biggest advantages of a properly structured Manulife One mortgage is flexibility.

Life doesn’t always follow a perfect budget.

Sometimes:

a roof needs replacing

a furnace fails

someone is off work for a period of time

or an unexpected expense shows up with no warning

With Manulife One, the equity you’ve built is easily accessible when you need it.

That means you can:

use available equity to handle short-term life events

avoid high-interest credit cards or emergency loans

and keep everything in one place

Just as importantly, once things settle, you can get right back on track with paying the mortgage down using the same cash-flow-first structure.

You’re not “breaking” the mortgage or resetting your entire plan, you’re temporarily using flexibility that was built into the structure from the start.

Kowing it’s there if you need it, creates peace of mind for many homeowners.

One of the biggest benefit isn’t just the interest savings, it’s knowing you have a mortgage that can adapt when life changes.

Who Is a Manulife One Mortgage Right For?

This tends to work best for homeowners who:

have equity in their home

have fairly steady income

usually have money left over after expenses

want flexibility and long-term efficiency

may want easy access to their equity now or in the future

It is not designed for:

People who spend everything they earn

or people relying on credit for basic expenses

For the right homeowner, it can be a powerful foundation to pay off your mortgage faster.

Want to See How This Would Work For You?

Understanding the structure is the first step.

The next step is seeing how it applies to you.

Watch the video training where i walk you through how this works using real homeowner numbers.

Key Takeaways

A Manulife One mortgage combines your mortgage, line of credit, and daily banking into one account.

It’s not a strategy on its own, it’s a tool that supports a cash-flow-based mortgage strategy.

The savings come from interest efficiency and faster principal reduction.

Fit matters more than features, this structure works best for homeowners with steady income and surplus cash flow.